So, the first picture I chose for this post was our mailbox lying on the ground after some kids ran into it.

The idea was something like, “Look at what you deal with when you buy a home.”

But my wife said the thumbnail kind of looked like a gun; and yes, she was right. So here we are instead.

This is Part 3 of an ongoing series reviewing the past ten years of our finances.

My footsteps crunched in the snow as I walked up the short sidewalk to our ground level apartment. I grabbed the mail out of the mailbox and as I did, my eye caught the music licensing company logo on the front. Cool! I had been spending a lot of time in the evenings producing and refining my music in hopes of landing corporate advertisement projects. My quarterly royalty check was inside, probably.

I tore the envelope open and blinked at the amount of the check. Wow. Nice. Suddenly my side hobby had become a little more than that. We were blessed in that our income had been rising, our apartment lease was coming up, and there was a rent increase looming. The housing market was down. Interest rates were down.

We were ready to buy a house.

In early 2012 we started looking. Our friends weighed in with their opinions. One in particular, who I respected very much in terms of his financial advice, recommended that we should continue to rent because of all the extra costs and complications that came with owning a house. If we followed his road-map, we would be millionaires before we knew it, he said.

His comment made me stop to think. We had piled up a decent amount of cash with which we could have taken a chunk out of our student loans. I knew that renting was wasting a lot of money, but I didn’t know how much.

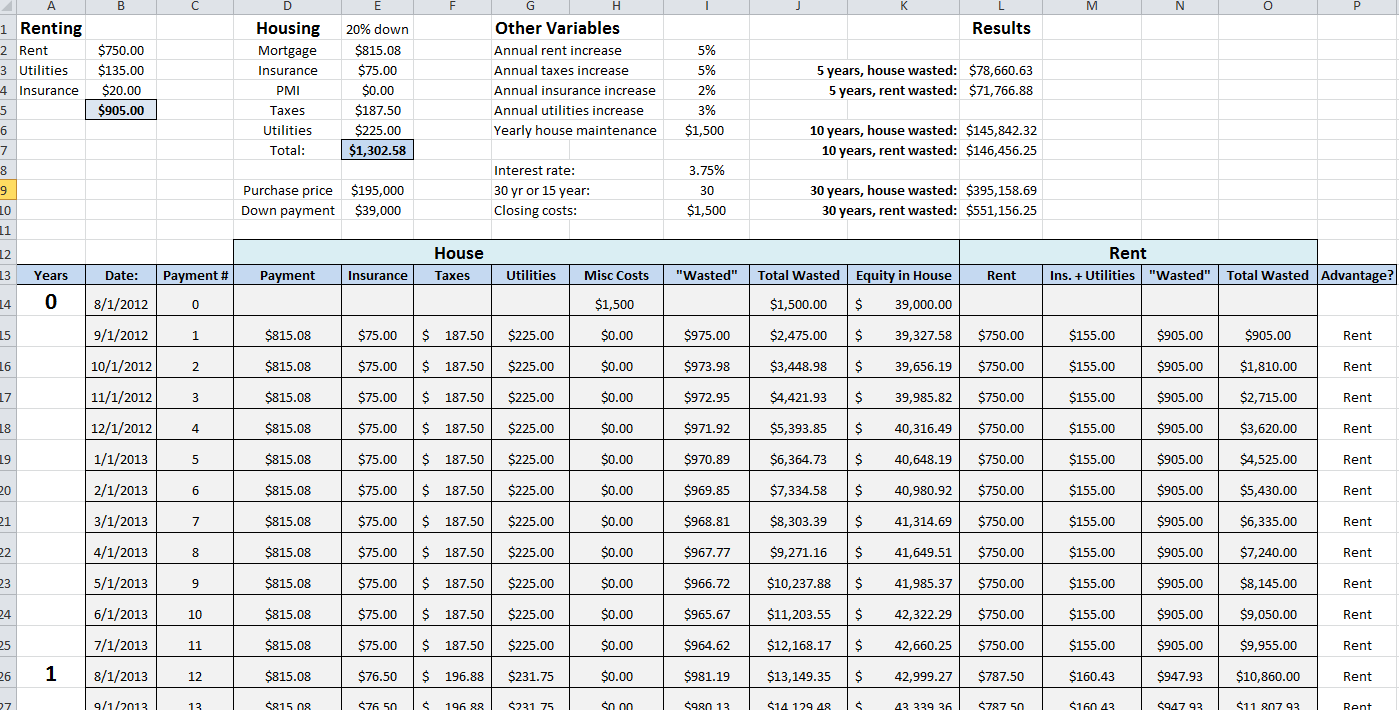

So I built a model to compare the costs.

I characterized “wasted” housing money as any money that wasn’t going toward equity. Now, I know that on a cold winter night, gas and electric utility usage seems to be anything but wasted, but it’s still an expense that doesn’t leave anything to show for it after the bill is paid. Regardless of how good that warm shower feels. Indeed, according this this definition, everything we would pay per month for housing, whether we would rent or buy, would be “wasted” except the principal part of a mortgage payment. In the model, I defined wasted money as follows, and built in certain assumptions:

Wasted Money

- Buy House: Interest portion of mortgage payment, utilities, insurance, property taxes, closing costs, maintenance, fixing window boxes after they fall off the house and other such things

- Rent: Monthly rent, insurance, utilities

Assumptions of the Model

- Rent would continue to increase an average of 5% per year. We were paying $750 per month at the time.

- Utilities would increase an average of 3% per year, taxes 5% per year, and insurance 3% per year.

- We would spend, on average, $1,500 annually for the house’s routine maintenance.

- The mortgage would be a 30 year mortgage at 3.75%, with 20% as a down payment (The 15 yr. vs 30 yr. mortgage decision deserves its own post).

The model.

So what did I find out? It’s probably easier to summarize the results by bullet points. (Numbers won’t match the screenshot, FYI.)

- Over 5 years’ time, purchasing a house would have wasted $1,262 less than purchasing the house.

- Over 10 years’ time, purchasing a house would have wasted $21,408 less than renting.

- The break-even point, where the wasted expenses would be equal whether renting or buying, was 4.6 years.

Other things I considered. There are, of course, other factors that played a part in this decision.

- We didn’t plan on my wife continuing to work for much longer, so I didn’t want to get into a house that we would be struggling to pay for once she stopped working.

- We didn’t want to mess around with buying a smaller home, and then selling and re-buying in a few years. For some people, this sounds fun and exciting. No thanks for us! We wanted to skip that step as much as possible, so we tried to jump to a home that could handle kids from the outset.

- Getting to a 20% down payment was a requirement. We didn’t want any PMI.

- 30 yr. vs 15 yr. mortgage makes a difference, of course. (The house vs rent savings with a 15 year mortgage at 5 and 10 years become $10k and $50k). I’ll explain why I chose a 30 yr. mortgage in a future post.

- The house would probably appreciate roughly 3% per year.

- The obvious non-cash related benefits. The house was considerably larger. Starting a family would not be a fun adventure in our apartment. Our small group at church would have another possible place to meet.

- We hadn’t paid off all our student loan and vehicle debt yet.

- I viewed the tax deduction for mortgage interest as a bonus. It didn’t play a factor in our decision. (And we’ve lost it since, when the the standard deduction was recently increased as high as they did).

- As the years go on in the mortgage, I would be paying with dollars that have become worth less and less, due to inflation. Yet my payment is locked in at that lower rate. This is a good thing!

- From a cashflow perspective, even if less and less of the payments on the back end of the mortgage are “wasted” (since they are going to principal), there is still a cashflow impact. After some time, the “Rent vs Buy” question then becomes an “Invest vs Pay Down House Quicker” question. We’ll discuss this later also.

Our decision? We did buy the house. We aren’t robots who are perfectly financially rational decision-makers. Life isn’t purely about squeezing every penny out of every decision. In a world of perfect investment decisions, continuing to rent for a few years would have meant being able to pay down student loans quicker, which would have saved us 6% for each of those payment. That number, though, isn’t the true gain, since the appreciating value of the house we bought and the house savings I calculated above would reduce that opportunity cost.

![]() In Retrospect, What Was Good: The model helped me to get an understanding of how much house we could comfortably afford without over-extending ourselves. It gave us a “max” that we wouldn’t got over. I’m happy with our decision, which landed us with a house payment around 17% of our gross income and about 25% of net at the time of purchase. We wanted to buy a house and originally thought that we could go bigger. (The bank suggested that we go $100k bigger!) Building this model helped me to dial down our our expectations. It’s very easy to underestimate costs when emotionally leaning toward a decision. The model was reasonably close to actual expenses. (The 2012 model overestimates our cost today, this current year 2018, by about $100/mo. Not too shabby.

In Retrospect, What Was Good: The model helped me to get an understanding of how much house we could comfortably afford without over-extending ourselves. It gave us a “max” that we wouldn’t got over. I’m happy with our decision, which landed us with a house payment around 17% of our gross income and about 25% of net at the time of purchase. We wanted to buy a house and originally thought that we could go bigger. (The bank suggested that we go $100k bigger!) Building this model helped me to dial down our our expectations. It’s very easy to underestimate costs when emotionally leaning toward a decision. The model was reasonably close to actual expenses. (The 2012 model overestimates our cost today, this current year 2018, by about $100/mo. Not too shabby.

![]() In Retrospect, What I Would Have Changed: Not much. We got in at a 3.75% interest rate, for a reasonable price, landing a house payment that is currently 12% of our gross income. We skipped the “starter house” size in order for our family to be able to grow into the house for some time. Had we not wanted to have kids, though, continuing to rent and pay down loans would have probably been the better choice. Back to what I said earlier about non-financial factors that help make decisions for us!

In Retrospect, What I Would Have Changed: Not much. We got in at a 3.75% interest rate, for a reasonable price, landing a house payment that is currently 12% of our gross income. We skipped the “starter house” size in order for our family to be able to grow into the house for some time. Had we not wanted to have kids, though, continuing to rent and pay down loans would have probably been the better choice. Back to what I said earlier about non-financial factors that help make decisions for us!

![]() Have you bought a house? Are you currently renting? How are you weighing your decision?

Have you bought a house? Are you currently renting? How are you weighing your decision?

{kind=link}

Leave a Reply